In line with annual speed book news, Financial institution has brought it a step then by reworking and you can initiating its mortgage prices structure. It a big earn to own customers since it indicators cheaper money minimizing interest rates.

In accordance with annual rate book updates, Lender has had it one step next because of the reworking and unveiling its home loan rates build. It a massive winnings having users because it indicators minimal costs minimizing interest rates.

Recently Justmoney looks at what this signifies to possess Southern African residents, existing and potential, and just how this will help them cut.

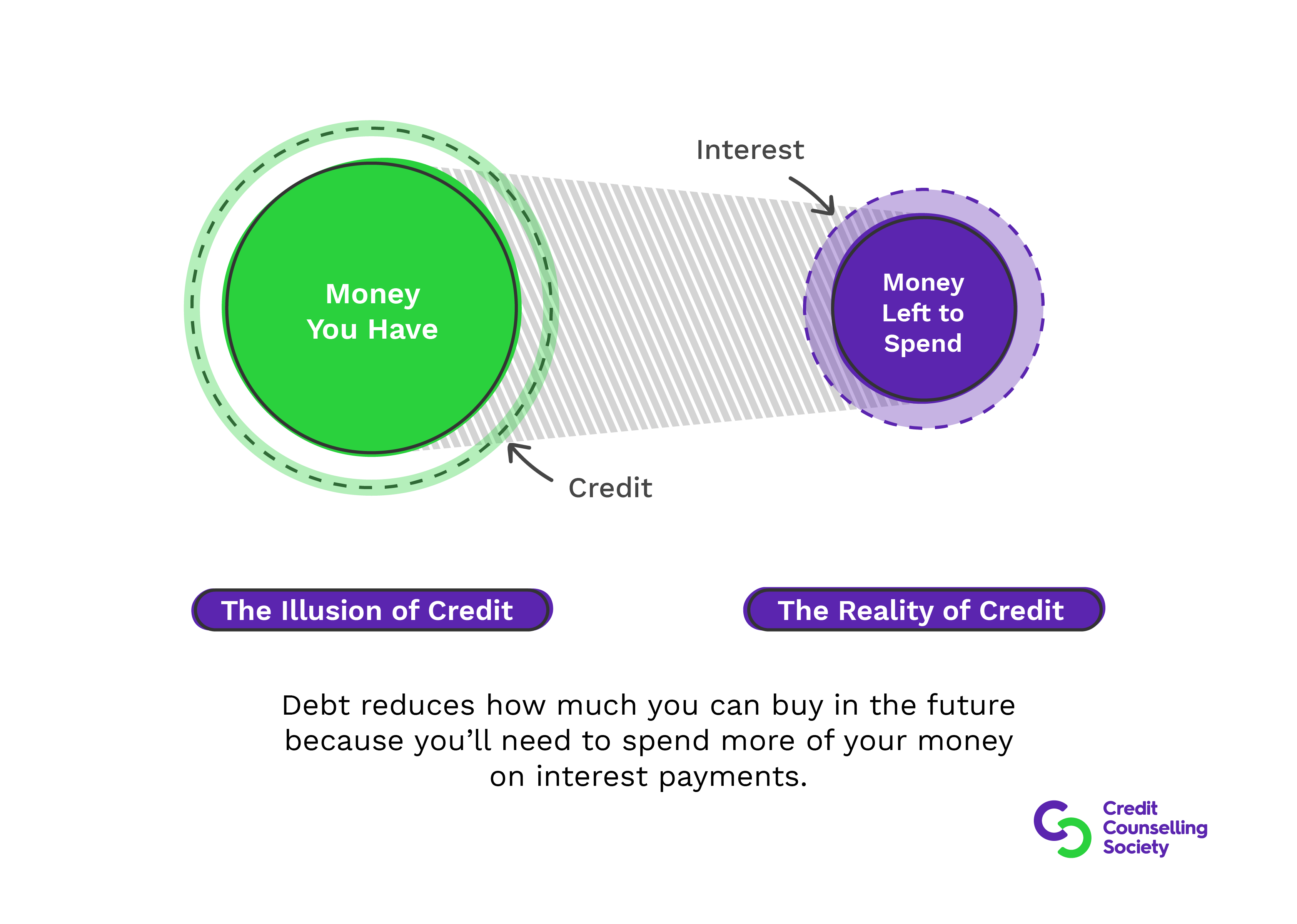

A traditional home loan typically has a single interest rate, usually linked to perfect, which is supplied in the the start of one’s loan and applicable from the label.

The minimum month-to-month instalment reduces as mortgage are paid down

Within the latest structure the pace relevant towards mortgage, while you are nevertheless about best, try tiered into about three classes. Such kinds was determined by just how much resource could have been paid, says Andrew van der Hoven, direct out-of home loans on Lender.

Considering van der Hoven that is best portrayed by way out of an illustration: Regarding a bond to possess R1,000,000 over 2 decades from the tiered rates framework the eye price can be as pursue:

This new part of the mortgage ranging from R800,000 and you can R1,000,000, are certain to get an interest rate away from % (finest + 0.25%). The brand new part of the mortgage between R600,000 and you may R800,000, gets an interest rate regarding % (prime), while the portion of the mortgage anywhere between R0 and you may R600,000, will have an interest rate of % (perfect 0.25%).

Because a customer takes care of his financing the brand new weighted price often consistently eliminate up until they has reached a reduced level out-of ten% (prime 0.25%). Thus giving people a bona fide loss in its instalment month-to-month and you may for the interest, preserving all of them currency compared to a vintage financial, says van der Hoven.

To phrase it differently, the consumer is not repaired to at least one rate of interest at the the newest inception of mortgage while the a lot more the client pays off of the home loan, the lower the pace is.

In the example during the period of twenty years, this customers will save over R67,000 inside focus than the a traditional single price loan priced at the same speed of %, states van der Hoven.

Furthermore, in the event that a consumer features more finance to invest towards household loan, the client can benefit off a lesser speed together with discounts was even more. Ultimately, the more a buyers pays new less the guy pays for the focus, he explains.

The pace minimizes while the financing is actually reduced. The customer isnt trapped on a single price for the life of its financing any more.

- Clients are compensated which have a lower life expectancy interest rate once they put a lot more loans bad credit personal loans NV each time during the term.

While you’ll find conditions, speaking of smaller than average tend to be strengthening, development, cost inclusive, vacant belongings, and you can loans with more than 40% deposits or even in title out of a juristic individual. Plus, would be to a consumer not want an excellent tiered rate build and like a single speed this might be and nonetheless offered, adds van der Hoven.

The guy went on, including that the fresh price is designed to reward readers having every payment they make on their travels on the owning their home.

Adrian Goslett, President and local director of Re/Maximum of South Africa, claims you to definitely Basic Bank’s home loan restructuring was a particular earn to possess property owners.

Ultimately, while the customer pays along the mortgage the speed tend to drop-off

The bank has given by itself an edge more its opposition with it flow. Making it likely that almost every other creditors often either features to check out Simple Bank’s analogy or manage designs of their own to help you compete, according to him.

Van der Hoven contributes that they accept that owning a home is important to money development and they desire to be section of you to travel. Financial institution do not chat for the competitors, but we create trust that it strongly encourages home ownership.